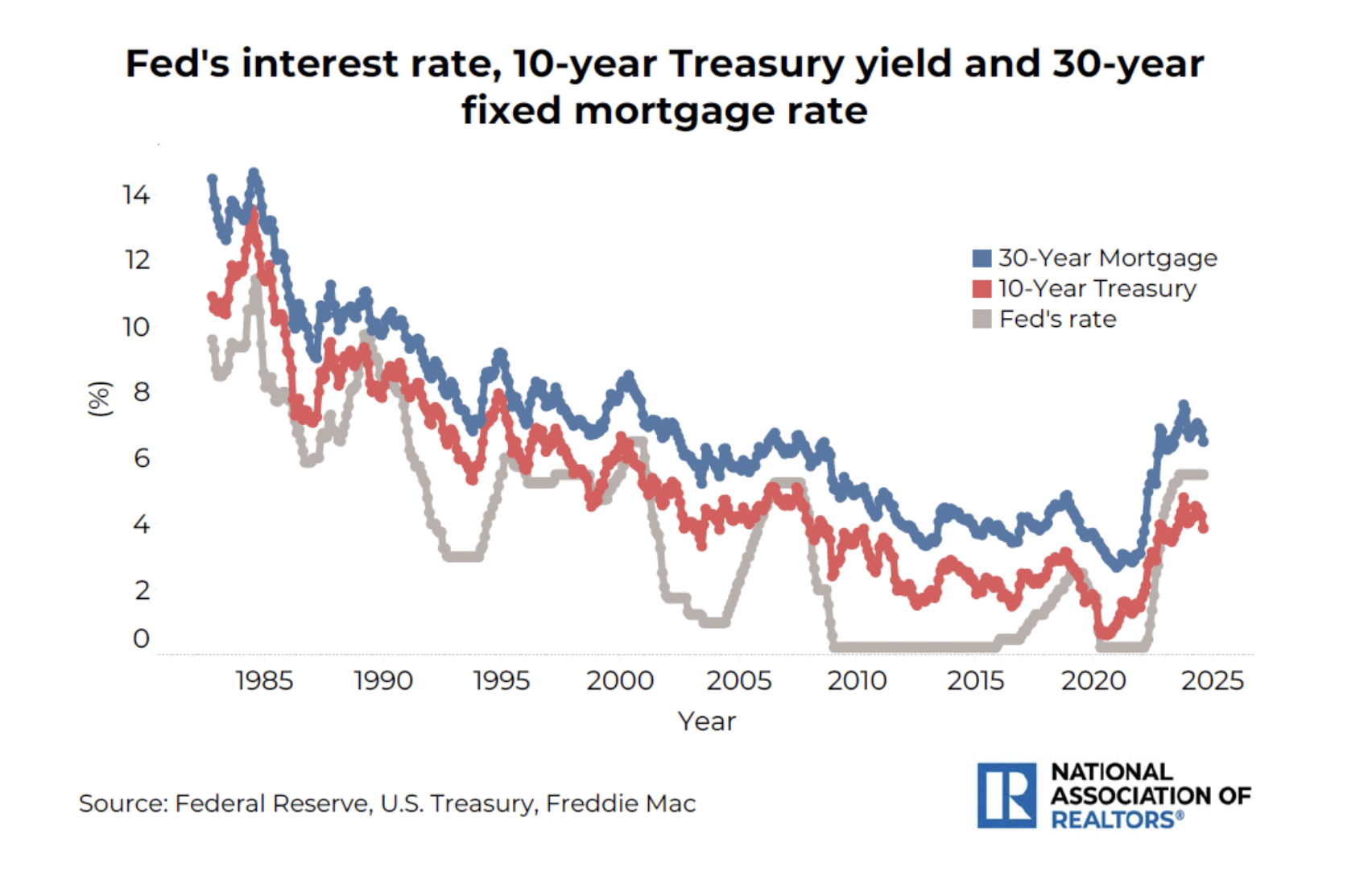

s and mortgages. When the Fed adjusts its rate, it triggers changes across the broader lending system.

The expectation of a Fed rate cut typically pushes down long-term rates like the 10-year Treasury yield, which is closely tied to the 30-year fixed mortgage rate. This is why mortgage rates tend to decline in anticipation of a Fed rate cut, even before it officially happens.

Historically, the market responds to expectations, not just actual Fed decisions. Data shows that both the 10-year Treasury yield and mortgage rates usually start trending down a few months ahead of an anticipated Fed rate cut. Here are a couple of examples:

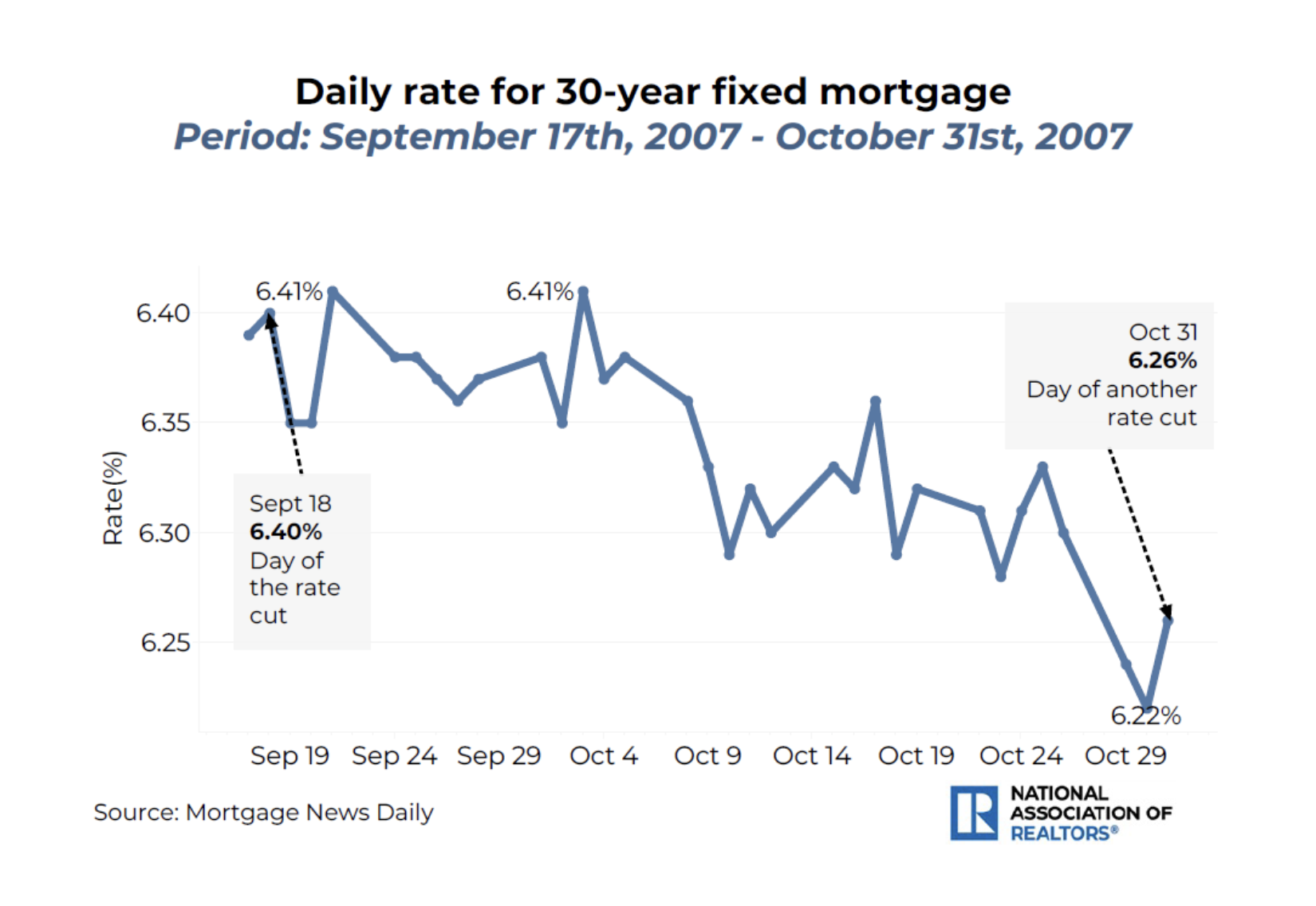

Rate cut on Sept. 18, 2007

While the Fed cut its rates in mid-September 2007 after holding them at the same level of 5.3% for 14 months the 10-year Treasury yield had already begun to decline in July and August, ahead of the cut. Specifically, after surpassing 6.7% in mid-July, the 30-year fixed mortgage rate had already dropped to 6.4% by the day before the actual rate cut. On the day of the cut, mortgage rates ticked up, only to drop to 6.35% over the next couple of days before hovering around 6.38% for the next ten days or so. Rates fell below 6.3% on October 10 in anticipation of the Feds next rate cut on October 31.

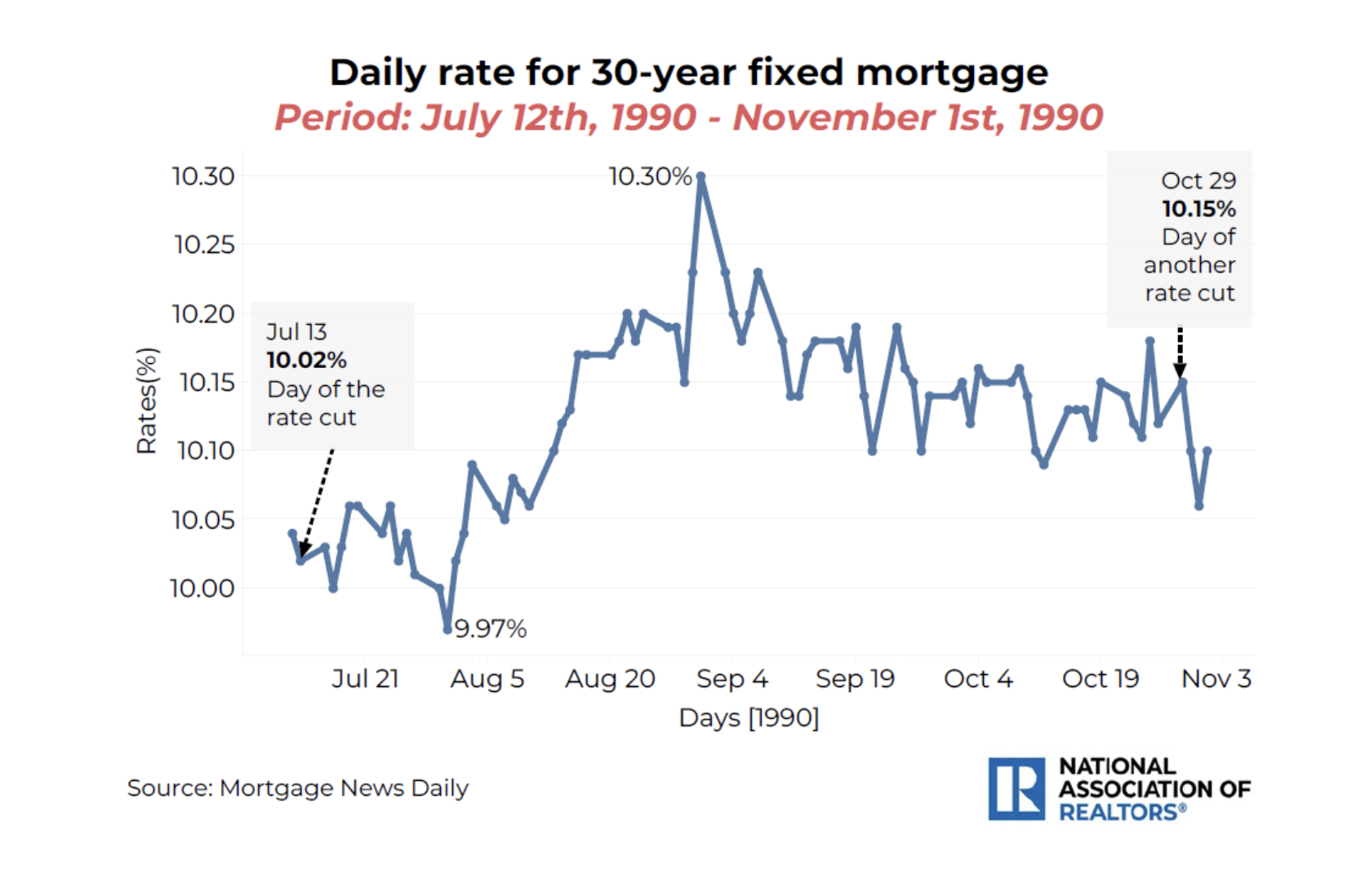

Rate cut on July 13, 1990

In July 1990, the Fed lowered its rates, while a couple of months earlier, the 10-year Treasury yield and mortgage rates had already started to fall. After reaching 10.49% on May 10, mortgage rates had already dropped to 10.02% by the day before the cut. On the day of the cut, rates ticked up to 10.03%, and mortgage rates didnt experience a significant drop afterward. In fact, they rose above the levels seen in July but eventually fell below the 10% threshold following an additional rate cut from the Fed on October 29, 1990.

We are seeing the same pattern now. Although the Fed has not yet cut rates, the 10-year Treasury yield has been easing since May, and the 30-year fixed mortgage rate has followed suit since June. Mortgage rates are over 100 basis points lower than they were on May 29th. This suggests that markets have already priced in some of the expected impact of the Feds upcoming rate cut. Thus, homebuyers shouldnt wait until September 17 the expected day of the cut in the upcoming Fed meeting to purchase their house if they have already found the right home.

How low could mortgage rates fall after the cut?

This is a very challenging question. Predicting mortgage rates is difficult due to the complexity and interplay of various economic factors that influence them. However, in very simple terms, historical data suggests that a 100-basis point rate cut typically leads to an 87-basis point drop in mortgage rates. With the Fed expected to lower its rates by 50 basis points by the end of the year, mortgage rates could fall to around 5.9% by years end. Nevertheless, this impact will likely be lessened as mortgage rates have already priced in some of the expected rate cuts. As of now, mortgage rates are already over 100 basis points lower than they were at the end of May 2024.

Five things homebuyers should consider after the rate cut:

Lower mortgage rates:One of the most immediate effects of a Fed rate cut is the potential for lower mortgage rates. For prospective homebuyers, this can mean lower monthly payments or the ability to buy a more expensive home than they otherwise could. However, as analyzed above, mortgage rates have already priced in some of the effects of the Feds rate cut. This could mean rates may not fall significantly after the cut next week.

Easier qualifications for mortgages:When mortgage rates fall, the interest portion of monthly payments decreases, which lowers the total payment. This makes it easier for more borrowers to meet lenders' debt-to-income (DTI) ratio requirements and qualify for mortgages that may have been unaffordable at higher rates. Additionally, with lower rates, lenders consider borrowers less risky since the smaller monthly payments reduce the chances of default. Lower rates not only help the process of qualifying for a new mortgage but also allow homeowners to refinance. In 2023, 74% of mortgage originations for home purchases carried rates above 6% (2.6 million mortgages), along with 82% of home improvement loans (493,230 loans) and 75% of refinances (812,140 refinances).

Stronger demand for housing:Lower mortgage rates reduce the cost of borrowing, increase purchasing power, and create a sense of a rush to secure a lower rate, all of which tend to drive up housing demand. However, in many areas where housing inventory is already low, this boost in demand can lead to more competition among buyers. The downside of increased demand is that it puts upward pressure on home prices as multiple buyers compete for a limited number of homes. In markets with ongoing housing shortages, this price increase can offset some of the affordability gains from lower mortgage rates.

Improved housing affordability:Home prices and mortgage rates are the two main components that define a mortgage payment. The home price determines the principal amount borrowed, while the mortgage rate affects the interest paid on that principal. Thus, any changes in either of these factors substantially affect the overall monthly mortgage payment. In the meantime, in a previous NAR analysis, data suggests that between these two factors home prices and mortgage rates - decreasing mortgage rates can more swiftly improve the affordability of homes compared to lowering house prices. A one percentage point decrease in mortgage rates can reduce the monthly mortgage payment mortgage rates as much as a 10% reduction in home prices. However, in areas with a severe housing shortage, lower mortgage rates could be offset by higher home prices, as lower mortgage rates are expected to increase housing demand.

More inventory in the market:Affordability is interconnected with the availability of homes. Better affordability also results in more affordable options. According to a recent NAR analysis, with lower mortgage rates, buyers at all income levels can afford a greater number of listings, thereby expanding their choices. The impact is more pronounced at certain income levels, particularly in the middle and upper-middle income brackets ($75,000-$150,000). For higher income levels ($150,000 and over), the percentage increase in affordability is smaller because they already have access to a majority of the housing market. Higher-income levels are also less sensitive to rate changes.

In addition, the gains from lower mortgage rates could be even larger, as expected rate reductions could encourage more homeowners to sell, thereby increasing the overall housing inventory.

Furthermore, a Fed rate cut can also positively affect the construction industry. Lower borrowing costs make it cheaper for developers to finance new projects, potentially leading to increased construction of new homes.

Therefore, if youve already found a home that fits your needs and budget, theres no need to wait for the official rate cut. This may help you avoid increased competition, and you can always refinance if rates drop significantly.

When you are ready to buy or sell your next home, please call me, Marie McLaughlin 727-858-7569.

Source: https://www.floridarealtors.org/news-media/news-articles/2024/09/upcoming-rate-cut-5-things-consider